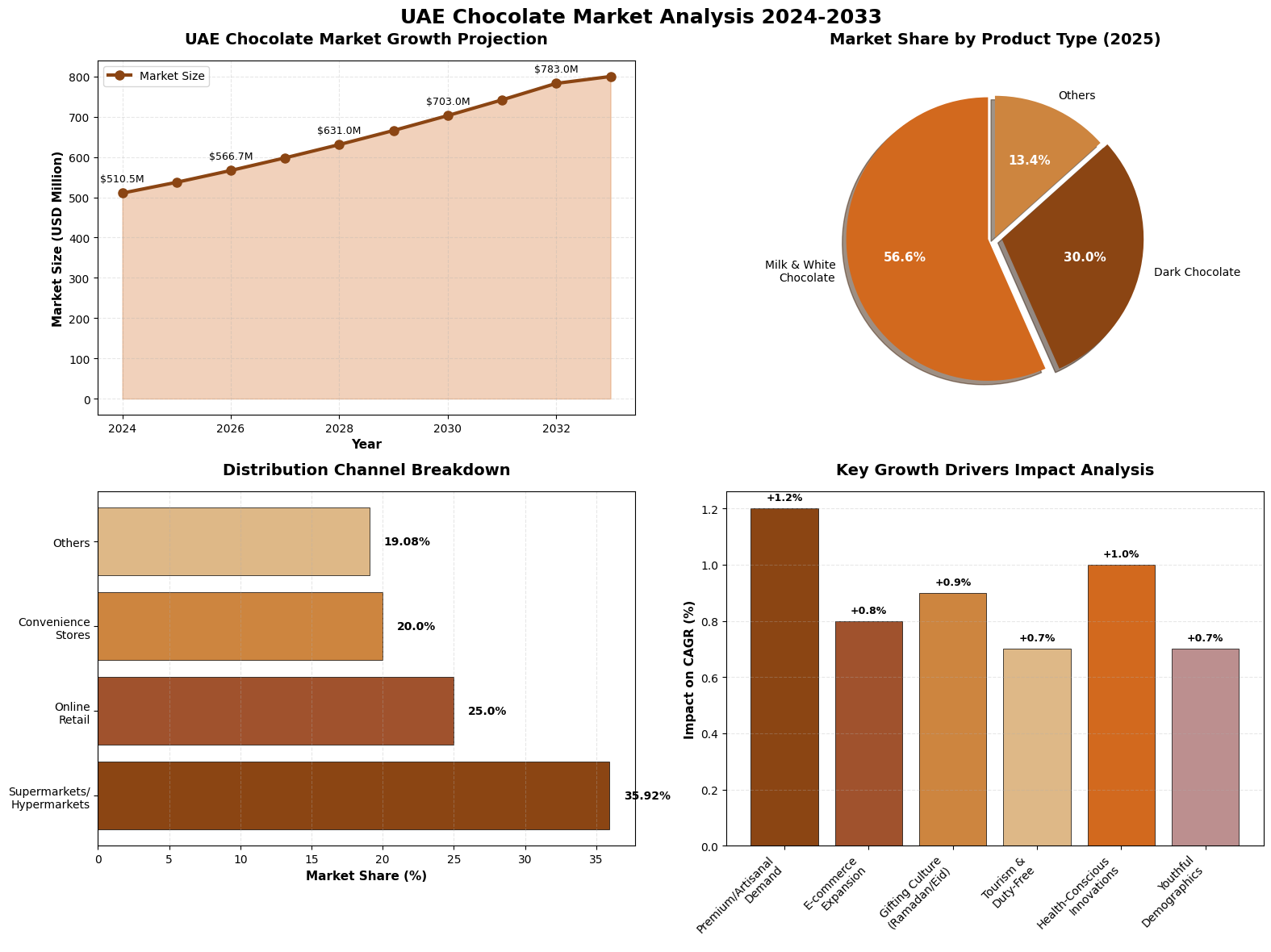

The UAE chocolate market has demonstrated remarkable resilience and consistent growth despite global economic challenges. Starting from a valuation of USD 537.30 million in 2025, the market reached USD 566.68 million in 2026 and is projected to achieve USD 739.39 million by 2031, growing at a compound annual growth rate (CAGR) of 5.47%.(DiMarket)

This steady expansion occurs even as cocoa prices nearly doubled between 2024 and 2025, highlighting the sustained demand for premium and artisanal chocolate products in the UAE. The market appears less affected by fluctuations in raw material costs, particularly in the premium segment where consumers prioritize quality and brand prestige over price considerations.

Different research firms provide varying estimates, reflecting different methodologies and segment focus:

Note: Variations in projections stem from differences in market segmentation, data collection methods, and inclusion of industrial vs. retail chocolate sales.

The UAE chocolate market features a dynamic competitive landscape with both international giants and distinguished local artisanal brands. The market demonstrates moderately high concentration, with major multinational corporations dominating mass-market volume while premium and gifting segments are led by specialized luxury brands.

Leading mass-market player with popular brands including M&M’s, Snickers, Twix, and Milky Way. Strong presence in supermarkets, hypermarkets, and convenience stores across all seven emirates.

Established a new regional headquarters in Downtown Dubai in February 2024, expanding workforce from 12 to over 400 employees. Aims to double GCC business within five years with brands like Ferrero Rocher, Nutella, and Kinder.

Major presence with Cadbury Dairy Milk and other confectionery brands. Strong focus on localized marketing and seasonal assortments for regional festivals.

Introduced premium “Les Recettes De L’Atelier” line in UAE featuring sustainably sourced cocoa and exclusive flavor profiles. Partnered with Dubai AI Campus in 2024 to develop AI tools for identifying product innovation opportunities.

Inaugurated flagship boutique in Dubai Mall showcasing dark and milk chocolates with live chocolate crafting workshops. Released limited-edition “Dubai Style Chocolate” bars in Europe in 2025 that sold out within hours. Launched official UAE e-shop in March 2025.

Opened chocolate café and retail outlet in Dubai Mall in September 2024, showcasing the UAE’s first chocolate fountains. Strong presence in luxury gifting segment with iconic gold boxes.

The World’s First Camel Milk Chocolate

Founded in Dubai in 2008, Al Nassma produces unique luxury chocolates using camel milk, which contains less fat and more vitamins than cow’s milk. Signature products include “Arabia” blend with cardamom and cinnamon, and macadamia-orange bars. Available at Dubai Duty Free and hotel boutiques.

Award-Winning Bean-to-Bar Artisan

Dubai-based chocolatier sourcing high-quality cocoa beans from Vietnam, Madagascar, Papua New Guinea, India, and Tanzania. Received five Academy of Chocolate Awards in 2025 for single-origin dark chocolate and vegan collections. Features Middle Eastern flavors including rose petals, saffron, figs, and dates. Uses traditional stone grinding methods over several days.

Lebanese Luxury Chocolatier

Operating elegant boutiques across UAE since the 1970s, Patchi is renowned for handcrafted pralines wrapped in luxurious packaging. Operates approximately 62 branches in Saudi Arabia and numerous locations in UAE malls and airports. Premium gift sets range from AED 75 to AED 1,185.

Premium Date and Chocolate Specialist

Backed by LVMH, Bateel plans to expand from 200 to over 500 stores by 2029. Specializes in premium dates dipped in chocolate and gourmet fillings. Product pricing ranges from AED 22 for Dubai Chocolate Bar to AED 1,185 for premium gift sets.

Luxury Gift Chocolate Brand

Known for handcrafted chocolates with sophisticated packaging. Popular choice for corporate gifting and special occasions.

Artisanal Chocolate Boutique

Offers premium handmade chocolates with unique flavor combinations and elegant presentation.

With a GDP per capita exceeding USD 43,000, the UAE possesses one of the world’s highest purchasing power levels. This affluence enables residents to treat chocolate not merely as a snack but as a luxury indulgence. Consumers in Dubai and Abu Dhabi prioritize brand prestige and ingredient quality over price, creating fertile ground for international luxury brands and high-end local boutiques to thrive.

As a premier global destination, Dubai alone attracts over 16 million international visitors annually. Tourism drives substantial chocolate sales through:

The UAE’s gifting culture during Ramadan, Eid, Diwali, National Day, weddings, and corporate events drives substantial demand for premium presentation and packaging. Chocolate is deeply integrated into hospitality and celebration customs across the multicultural population.

The 2024-2025 “Dubai Chocolate” trend featuring pistachio cream, tahini, and kataifi pastry generated over 120 million TikTok views and disrupted international markets. This viral success:

Health awareness is reshaping consumption patterns in the UAE:

Online retail is growing at 6.60% CAGR through 2031:

| Chocolate Type | Market Share (2025) | Growth Rate | Key Demographics |

|---|---|---|---|

| Milk Chocolate | 43% | Moderate | Families, younger consumers |

| Dark Chocolate | 40% | 7.51% CAGR (Fastest) | Health-conscious, affluent consumers |

| White Chocolate | 12% | Slower | Niche segment |

| Single-Origin | 5% | 6.70% CAGR | Premium consumers valuing traceability |

Countlines (snack bars) dominate due to the “on-the-go” consumption culture in urban centers like Dubai and Abu Dhabi, where portability and convenience are paramount. This segment is bolstered by social media-led impulse buying and single-serve portions appealing to Gen Z demographics who prioritize calorie control alongside indulgence.

Pralines and truffles experience significant growth at 6.74% CAGR (2026-2031), driven by popularity as premium gifting options during festive occasions.

The UAE market embraces regional ingredients that differentiate it from traditional European chocolate markets:

Leading retailers dominating chocolate sales:

These retailers attract consumers through extensive product assortments, competitive promotional pricing, and strategically placed impulse-purchase items at checkouts and end-caps.

E-commerce platforms are rapidly closing the gap with traditional retail through:

Luxury brands operate standalone boutiques in premium locations:

Dubai International Airport represents a significant channel for both local specialty chocolates (Al Nassma, Mirzam, Patchi) and international luxury brands, catering to 16+ million annual visitors.

Cocoa prices nearly doubled between 2024 and 2025 due to:

Additionally, the pistachio shortage driven by Dubai Chocolate trend and drought conditions in Iran and Turkey has increased ingredient costs for specialty products.

Abu Dhabi’s Nutri-Mark labeling system grades products on sugar and fat content, prompting producers to reformulate toward darker or reduced-sugar profiles to meet health standards and consumer expectations.

Desert climate and absence of local cocoa farming necessitate:

The market faces competition from both established global brands and emerging artisanal players, requiring continuous innovation in flavors, packaging, and marketing strategies.

Premium chocolate segment is projected to grow at nearly 7% CAGR through 2030, significantly outpacing mass-market trajectory. This shift reflects:

Growing trend toward establishing local production facilities:

Consumers increasingly prioritize:

Dubai Chocolate trend demonstrates potential for flavor profile expansion into:

The UAE chocolate market presents significant opportunities for growth and innovation in 2026 and beyond. With projected growth to USD 739.39 million by 2031, the market is characterized by:

Success in this market requires understanding the sophisticated, multicultural consumer base, investing in quality and innovation, and leveraging both traditional retail and emerging digital channels. The UAE’s position as a chocolate trendsetter, demonstrated by the viral Dubai Chocolate phenomenon, underscores its strategic importance in the regional and global chocolate industry.

| Product | Application | Specification |

| Alkalized Cocoa Powder | Chocolate beverages, ice cream, baked goods | 10/12% & 20/22% fat, various pH levels |

| Natural Cocoa Powder | Premium baking, health products | High-flavanol, single-origin options |

| Cocoa Butter | Chocolate manufacturing, cosmetics | Deodorized and natural grades |

| Cocoa Liquor/Mass | Industrial chocolate production | Various cocoa origins |

| Chocolate Couverture | Artisan and industrial use | Dark, milk, and white varieties |

About Radad International: RADAD International is a leading global supplier of premium cocoa products, serving chocolate manufacturers across the Middle East, including the UAE, Saudi Arabia, and Kuwait. With decades of expertise in cocoa sourcing, processing, and logistics, we provide consistent quality, competitive pricing, and exceptional technical support to help our clients succeed in dynamic markets.

For more information about market opportunities, partnerships, or chocolate products, please contact Radad International.

Disclaimer: Market data and projections are based on available industry reports and research publications. Actual market performance may vary based on economic conditions, regulatory changes, and consumer behavior shifts.